Qualifying for a small business loan can significantly impact your business, but it’s not guaranteed. Lenders carefully evaluate several factors before approving a loan. One of the most critical elements is your credit score; a strong personal score above 680, alongside a healthy business credit profile, greatly enhances your chances. If your credit report contains any errors, addressing these promptly can also work in your favor.

Additionally, lenders typically favor businesses that have been operational for at least two years, as this demonstrates stability and a proven business model. Startups, however, might find the process more challenging unless they can showcase strong financials or collateral.

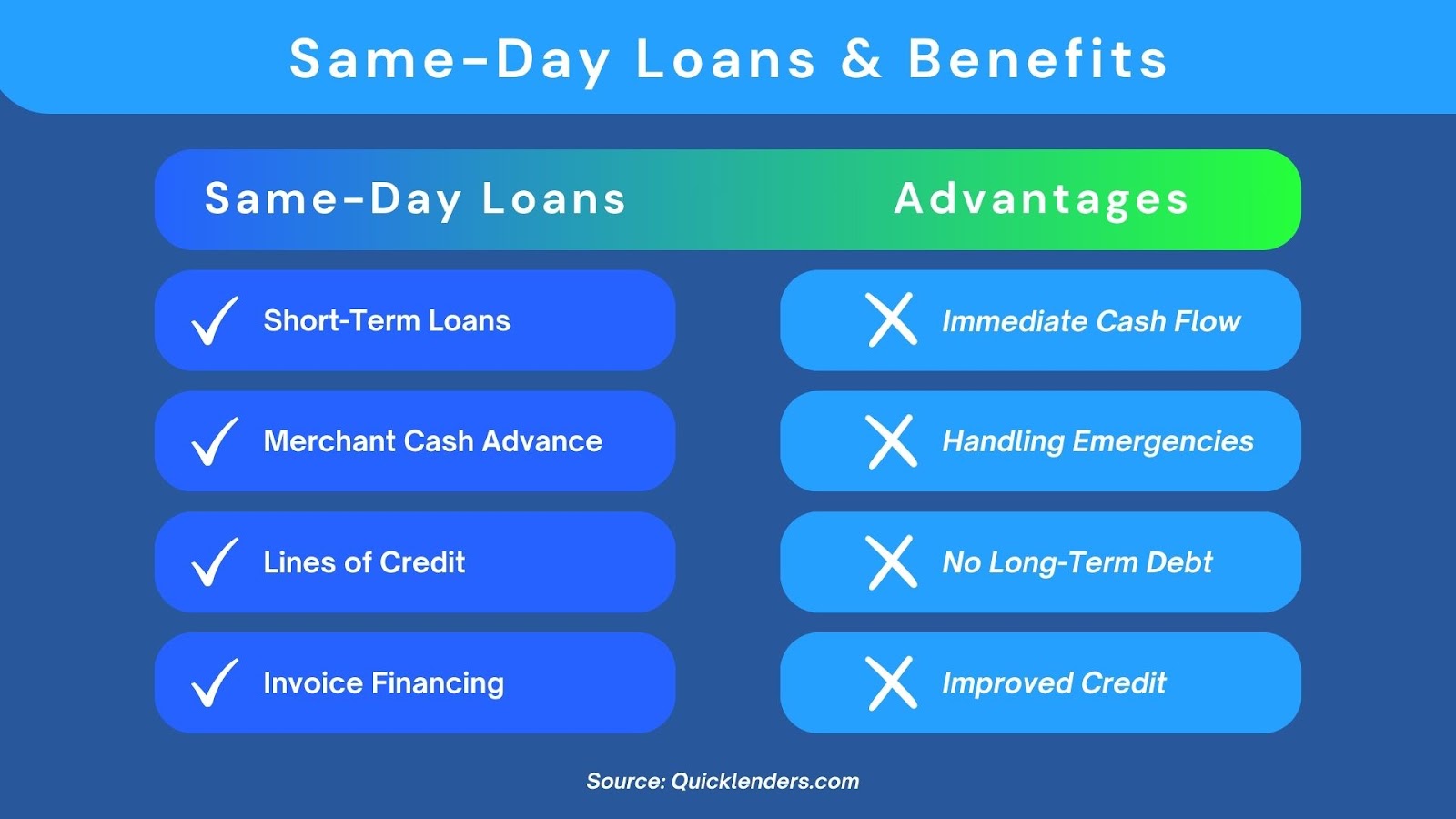

Common Types of Small Business Loans Explained

Finding the Right Loan for Your Needs

There are various types of small business loans available, each designed to meet different financial needs. Here are some of the most common types:

• Term Loans: A lump sum of money is provided upfront and repaid over a fixed term with interest. Ideal for major purchases or long-term projects.

• SBA Loans: Backed by the U.S. Small Business Administration, these loans offer low rates and longer terms but have strict qualification criteria.

• Equipment Loans: Specifically used to purchase business equipment, these loans often use the equipment itself as collateral.

• Invoice Financing: Allows businesses to borrow against unpaid invoices, helping improve cash flow without waiting for customers to pay.

• Merchant Cash Advances: Provides a lump sum in exchange for a percentage of future credit card sales. These are easy to qualify for but come with high fees.

Choosing the right loan depends on your business’s needs, financial health, and how quickly you need access to funds.

How Interest Rates Affect Small Business Loans

Interest rates are a key factor that influences the total cost of small business loans, and understanding how they work can save you a substantial amount in the long run. Most loans offer either fixed or variable rates. Fixed rates remain constant throughout the loan term, providing predictable monthly payments that simplify budgeting. Variable rates, on the other hand, fluctuate with market conditions, which can lead to lower initial costs but also pose the risk of increased rates over time. Several factors influence the rate you’ll receive, including your credit score, business financial health, loan amount, and term length.

Step-by-Step Guide to Applying for a Small Business Loan

Applying for a small business loan can seem daunting, but knowing the steps involved can simplify the process. Start by defining the exact amount you need and how the funds will be used, as having a clear purpose strengthens your application. Before approaching lenders, ensure that you meet their eligibility requirements, such as minimum credit score, revenue benchmarks, and time in business.

Gather all necessary financial documents, including recent financial statements, tax returns, bank statements, and a solid business plan that outlines how you intend to use the loan to drive growth.

ey.

Small Business Loans vs. Business Lines of Credit: Key Differences

Understanding the differences between small business loans and business lines of credit can help you decide which option best suits your needs:

• Loan Structure: Small business loans provide a lump sum upfront that you repay over time with interest, while lines of credit offer flexible, revolving access to funds as needed.

• Payment Terms: Loans have fixed repayment schedules, whereas lines of credit allow you to draw funds and repay at your discretion, usually with minimum payment requirements.

• Interest Rates: Business loans typically have fixed or variable interest rates applied to the entire loan amount, whereas lines of credit charge interest only on the amount drawn.

• Use Cases: Loans are ideal for large, one-time purchases like equipment or property. Lines of credit are better suited for managing cash flow fluctuations or covering short-term expenses.

Choosing between these options depends on your business needs, repayment flexibility, and how you plan to use the funds.

How to Improve Your Chances of Getting Approved for a Small Business Loan

Securing approval for a business loan for a small business often requires preparation and proactive steps to strengthen your application. Improving your credit score is one of the most effective strategies—this means paying down existing debts, avoiding late payments, and correcting any inaccuracies on your credit report. Maintaining strong, updated financial statements that demonstrate consistent revenue and positive cash flow will further reassure lenders of your business’s ability to repay the loan.